")

You’re neck high in debt and going completely crazy about what to do, where to begin, and how the heck you’re going to get yourself out of debt fast.

During my quarter-life crisis, one of the areas that were deeply affected was my finances. I was neck high in debt, I could barely afford the new apartment I just got and I needed to figure out how to eat and survive this drama.

For the first few months, I ignored my money troubles for the most part. I dodged credit collector calls, I experienced a mini panic attack whenever my phone rang and I simply wanted it all to be over.

I secretly wished that it would magically fall into place as time passed but I knew that if I wanted to breathe again, I needed to get my money act and mindset together.

After being tired of sleeping on my sofa or a comforter spread for 2 months, my back ached, I was tired of walking out with a smile, and I made the decision to make a scary phone call. And that was to a loan officer.

I know, trying to get out of debt, and yet I’m getting along. Bear with me, it’s getting good. You see that financial consultation taught me a few things about money management and taking control of my situation. When the loan officer asked me, how do I eat? I was partly taken aback and partly comforted that someone else understood my situation.

I think in other countries there is something called a credit score, but here we have something called a debt/credit ratio. And mine was sky high! And I needed to bring it down fast! I did get my $15,000 loan approved, my repayments spread across 3 years, became smaller and I got a much better grasp on managing my money and my debt.

Disclaimer: I must insert a disclaimer here to share that I am NOT a financial expert. These basic practices & tips I will share with you will help you to an extent, as these are financial practices I have done myself over the last 3 years consistently. I have never read a money book in my life, “I’m currently trying to read Tony Robbins – Money Master The Game, but the intro is so boring”, so in due time. If you want expert advice on managing your money, please do so. I will also like to add that you may throughout your life span have some form of debt unless you become financially independent or a billionaire. But managing your money game is the key to skipping the monthly bill call-induced panic attacks.

So, how do you get rid of your debt fast?

As I write this, I have to date in the last 36 months paid off approximately 70 percent of my debt and that was new debt. Not the initially mentioned 15K.

From different institutions inclusive of hire purchase plans, and loans “plural”, I accumulated a new debt amount of $44,000 in 2017. I know, sounds like a lot but with good reason. As of today June 1st, 2020, I’ve paid back $29,439 and remain a balance of approximately 14k. Huge milestone. Here’s how I did it.

The Steps I Took:

- Having Money dates.

- Tracking my debt who, how much, and when.

- Finding and creating additional income streams & saved where I can.

Step 1 – Your Money Dates

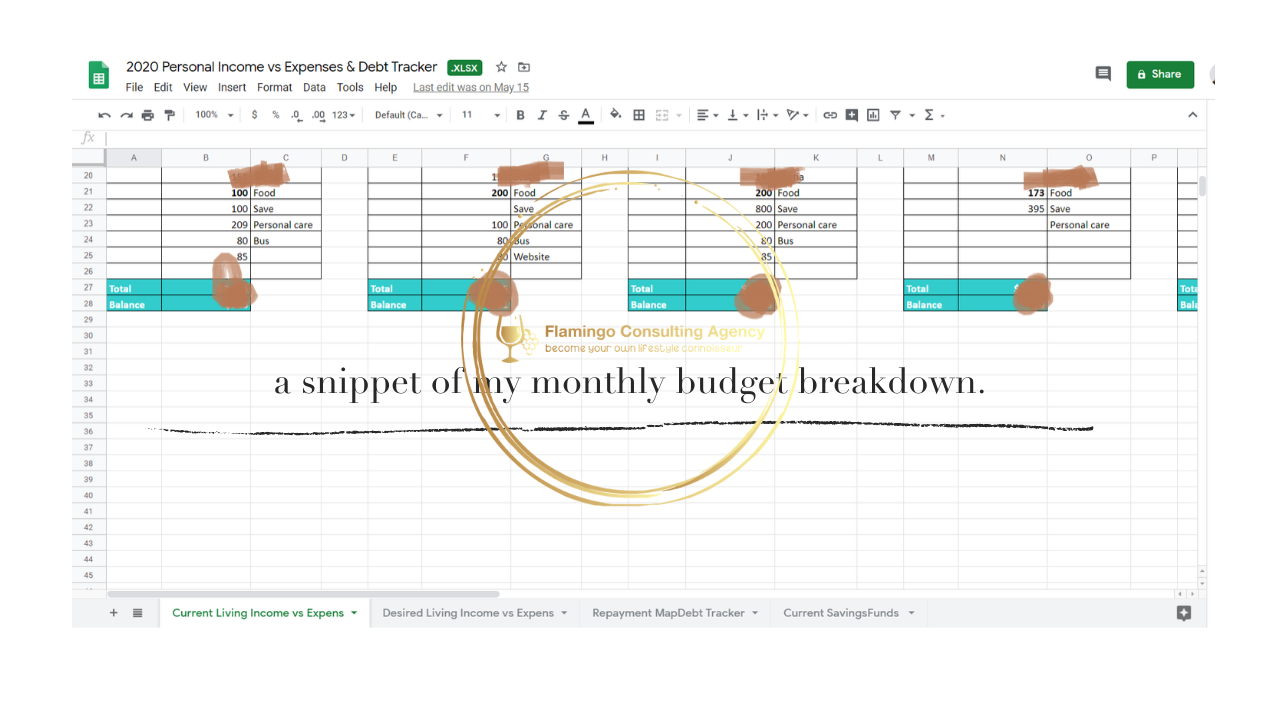

A money date ultimately leads to your Budget. Keeping an income vs expense budget has been one of the most life-changing games for me ever. I can tell you exactly how much tax, insurance, bills, rent, food, leisure, etc amount I have spent over the last 24 months if you were to ask me.

A money date is where you begin to make smarter financial decisions by taking stock of what’s happening and adjusting it to suit the results you want. For me, that included my online business expenses as I was not yet making a penny from it. For example, I canceled lead pages, and got resourceful with Squarespace & Mailerlite is pretty savvy. I learned some landing page tricks and voila. That’s $588 saved yearly.

Translate that into a budget.

Before keeping a budget, I constantly felt broke. I would wonder where in the hell was my money disappearing. I would get pain and 3 days later, cockroaches are having a party in my wallet.

Now starting a budget can feel like a task for someone who is afraid of facing money issues, or doesn’t have a habit of discipline. But start it nonetheless. If you know where your money is going, you have better control of it.

Budgeting also gives you leeway to cut back on unnecessary expenses, shift things around, and save, even if it’s $20. Don’t get crazy fancy with it, just get it done. If you can do this monthly, pretty soon, you will be a pro at it. You can also use a physical budget planner if you prefer.

So what do you put into your budget? EVERYTHING! The ice cream cone you purchased at lunchtime, the handbag you bought that you didn’t need, the electricity bill you haven’t paid. It all goes into your budget but in categories. And tracking it is the first step

Here’s an action step, for the next month, take track of every money transaction you make. For every physical receipt you receive, drop it into a jar on your dining table, if you don’t write it on a piece of paper and drop it into the jar.

At the end of the month, pour those receipts out, open a new spreadsheet, and create 2 columns. One labeled item, one labeled amount. Then categorize time. Food, leisure, medical, utilities, etc.

Tracking your expenses gives you a better understanding of where the measly $2 is disappearing to. And also, how quickly they mount into hundred-dollar bills. This might seem like a tedious task, but if you want to get your money game together, it will become fun!

Step 2 – Know your debt who, how much, and when!

This is where I got serious with my money. It’s a more concise breakdown of the budget tracking but also learning to play with money. Making it fun. Most people are afraid to face their financial reality, but unless you do, you can’t change it.

Unless you get intimate with the amount you owe down to the very detail it will feel like it’s always there.

It’s very conventional to shove the bills aside or steer clear of logging into your billing accounts.

YUP, you know what I’m talking about. The first step to financial freedom is not just making more money. It’s understanding where you are and accepting that for what it is.

When I made these investments they were with good purpose. I learned from the experiences they went to, and I enjoyed them. So I began to shift my mental approach to looking at my debt and embraced them.

Sometimes we can fall back on regretful sayings such as, I wish I didn’t take that loan. Or I wish I paid that bill instead. And sometimes, it’s with good measure. If you can’t afford to or do NOT NEED to, do not get a loan, credit card, or any form of financial obligation.

Financial Lessons – Saving when you live paycheck to paycheck.

In 2012, I learned about consolidating my debts, paying out earlier to save on interest payments, and NEVER taking out more than I can comfortably afford to pay back. I do not own a credit card “yet” and will not get one until I believe that I need to. For now, I am good with that.

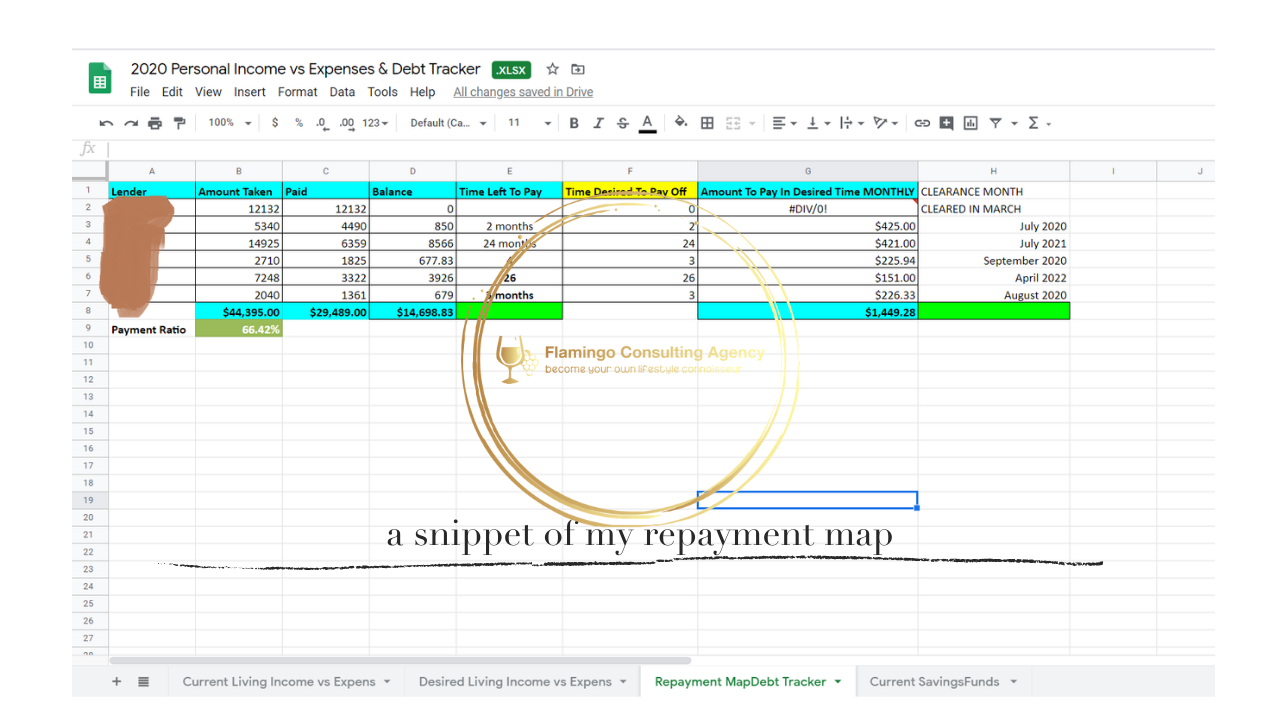

If you want to get your debt paid back fast, you must get strategic. This is where the game of spreadsheets and graphs comes into play. And you might not like this approach, so find an alternative.

In my monthly income and expense tracker, I have a sheet called my repayment map. This is where I track and update every single month, the amount I have paid out, the balance, and see where I can pay out earlier. In March of this year, I paid out my biggest lump 7 months in advance.

Don’t be afraid to have fun with it

I added a graph illustration as a fun approach for motivation to keep going, paying more than the minimum, and closing out in lump sums when I could to save interest. It can seem depressing in the beginning, but life-changing.

For example, If I knew that paying 5 months would equate to $5k, but If I saved 2 months’ worth of interest that would mean an additional 2k in my bank account.

The goal of the graph was to give me room to play with the numbers as I thought about the long-term benefits and not the short-term “pain” for a lack of a better word.

Get comfortable with understanding your payouts, and if you CAN afford to pay more than the minimum installment, or close it out earlier do so. You will breathe a little.

Step 3 – Creating or finding alternative sources of income.

Did you know that Youtube, Blogger.com, WordPress, Instagram, Facebook, etc are all breeding grounds for income generation? You’ve probably wondered how these bloggers make money. How do YouTubers get paid? How to start a money-making blog? It’s all doable, it can be a great alternative source of income to help you pay back your debt fast, but, it requires dedication and hard work.

When I first became a blogger, I had no idea that I could make money on it. Hell, I thought no one would see it. I thought it was a private journal but just online. Silly me. But that was way back in 2008.

Now I have NOT been consistent or actively pursuing sponsorships, ads, etc for my blog but I’ve made well over $2000 in the last 12 months from inbound requests only from it. Moving forward, however, this blog IS going to become one of my main streams of income.

I share this so that you understand that there are avenues to make extra income in your spare time. And it doesn’t have to be from a blog, YouTube, or an Influencer. Or You can get a second job after your 9-5 or on the weekends. Maybe clock some overtime.

You can create a course or a passive income digital product, or use a skill to provide a service through Upwork or Fiver.

One of my sisters provides VA, transcription, and audio recording services through Upwork & Fiver, oh, and you can start your own part-time business as I did with coaching.

Don’t forget to save a little, even if you’re in debt.

I know, save during debt. Here’s the thing, you don’t have to save a thousand dollars, or $500. As long as it’s something. The goal is to get into the habit of managing your money and saving is also part of the game.

Also, creating an additional source of income helps you save some more for uncertain times. Like right now.

If you need extra income and pay your debt faster in the process, NOW is the best time to up your game!

The technology industry and the e-commerce industry are booming right now and guess what, it’s going to continue that way.

As long as you get into the mindset and habit of educating yourself on money, controlling your spending, and managing your money you can pay your debt faster than you think.

It takes trial, error, and time.

Now I still have some financial cleaning up to do, but practicing these habits has helped me become savvier with my finances.

Creating a money mentality that’s powerful positions you far ahead in the game when it comes to accepting a debt AND enjoying your life.

You deserve to live your best life, invest in yourself, own your desires, and live without the fear of being in debt forever; and money is part of the game.

Do you have a massive amount of debt you’re trying to pay faster? Have you started with any of these practices? Join the conversation below & don’t forget to download the free sample income vs expense workbook below.

Pin This For Later

Subscribe to my Youtube channel,

Read This Post On Leveling Up Your Life

Read This Post On Renting Your First Apartment

xx Bisous.

Menellia.

")

")

")

")

")

")

")

")

")

")

")

")

")

")